Inside the Packaging Manufacturing Industry

A beverage brand in Austin was spending $0.18 per unit on folding cartons manufactured in Vietnam. Freight, customs, and a 20-day lead time were baked into the math. Then port congestion hit Los Angeles in early 2024 and their entire Q4 holiday run arrived six weeks late. The brand lost $340,000 in retailer shelf slots they could not fulfill.

That story is not unusual. It is, in fact, the defining tension of modern packaging manufacturing: the world’s cheapest production sites are not always the world’s most reliable ones. And the calculation of which factory in which country wins your business is far more complicated than a per-unit price quote.

So what actually determines where packaging gets made? Not in a surface-level way. I mean the real levers: the labor economics, the raw material geography, the regulatory regimes, the infrastructure gaps, and the geopolitical pressures that shift entire supply chains from one hemisphere to another.

This piece pulls back the curtain on all of it. Whether you are a small brand just starting to think about overseas sourcing, or a procurement director managing a multi-region supplier base, you will walk away with a sharper understanding of why your packaging is made where it is, and whether that should change.

Why Location Is the Most Underestimated Decision in Packaging Manufacturing

Most buyers think about packaging location in one dimension: cost. They get quotes from a domestic supplier and a Chinese manufacturer, see a 30% to 50% gap, and the decision feels obvious. But the unit cost is only one variable in a much larger equation.

Location determines lead times for products like custom gable boxes, which affect your ability to respond to demand spikes. It determines currency exposure, which affects your landed cost every quarter. It determines compliance risk, because a factory in a country without strong environmental regulations might produce materials that fail EU or US import standards. And it determines resilience, because a factory that is cheaper but concentrated in a single coastal region is one typhoon away from a six-week shutdown.

I have seen brands make location decisions based purely on per-unit price and later spend twice as much managing the downstream problems. The cost of a procurement mistake in packaging is almost always invisible in the spreadsheet and very visible in the P&L.

If you’re planning your supplier strategy, the guide below explains the full sourcing process.

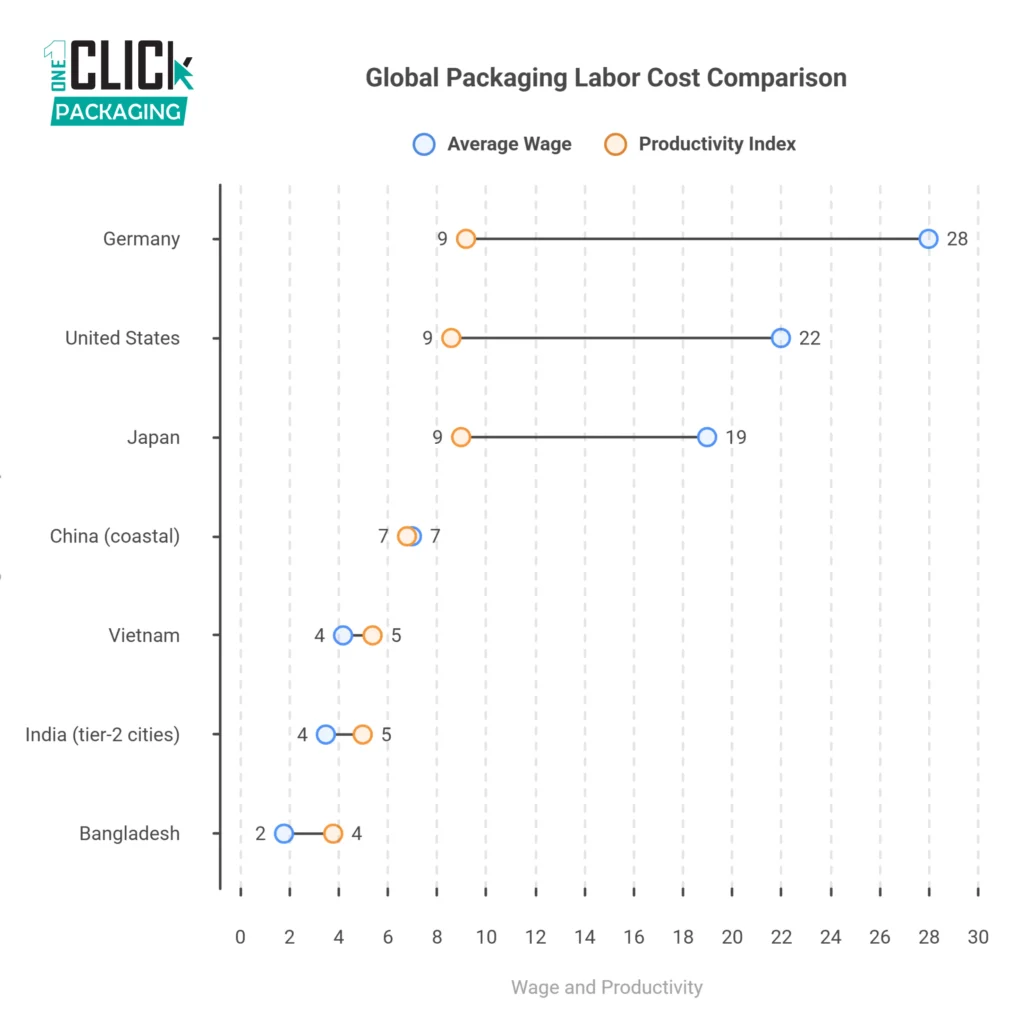

Labor Costs: The Most Obvious Driver and the Most Misunderstood One

Labor cost is the variable everyone cites first. Vietnam, Bangladesh, India, and China have historically offered manufacturing wages that are a fraction of what you would pay in Germany, the United States, or Japan. For labor-intensive packaging formats like folding cartons, flexible pouches, and hand-assembled gift sets, the wage differential can represent 20% to 40% of total production cost.

But here is what most sourcing guides will not tell you: labor cost without labor productivity is a meaningless number. A factory paying workers $4 per hour but producing 800 units per hour per line is not cheaper than a factory paying $18 per hour and producing 4,000 units per hour. The math has to include output, reject rates, and rework time.

Germany is the clearest example of this paradox. German packaging machinery, particularly from companies like Koenig and Bauer and MULTIVAC, is some of the most automated in the world. German converters can compete on complex, high-tolerance rigid packaging precisely because their wage-per-unit is offset by extraordinary throughput. They are not chasing labor arbitrage. They are using capital investment to eliminate labor as the cost variable entirely.

Where Wage Arbitrage Still Works in 2025 and 2026

For high-touch, labor-intensive formats, Vietnam and Bangladesh continue to offer meaningful cost advantages. Vietnam in particular has benefited from manufacturing migration away from China since 2018, when US tariffs under Section 301 began pushing brands to diversify. Companies like Sealed Air and Amcor have both expanded Vietnamese production capacity in the last four years.

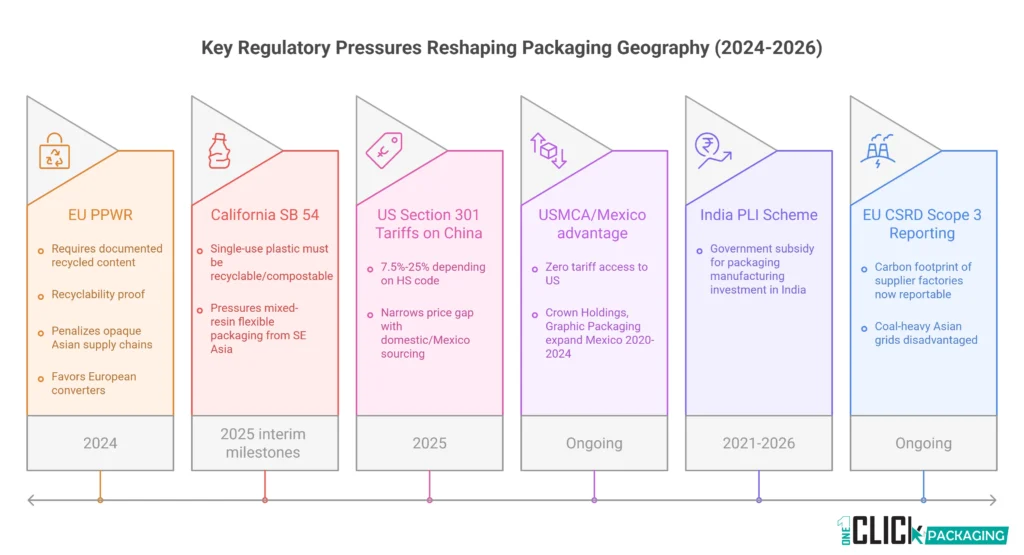

India is the most interesting story right now. Wage rates in tier-two Indian cities like Pune, Ahmedabad, and Coimbatore remain well below coastal Chinese equivalents, and the government’s Production Linked Incentive scheme has injected billions into domestic manufacturing capacity. The packaging sector specifically received PLI allocations in 2021 that have started to show up as real factory openings.

If you want to understand the deeper economics behind these shifts, the guide below explains how labor costs influence global packaging production.

See: How Labor Costs, Raw Materials, and Infrastructure Decide Where Packaging Is Produced

Raw Material Access: The Geography You Cannot Negotiate Around

A packaging factory is only as good as its raw material supply. And raw material access is determined by geography in ways that no amount of logistics spend can fully overcome.

Corrugated and paperboard manufacturing concentrates near forestry and pulp resources. Scandinavia, Canada, Brazil, and the US Pacific Northwest host major pulp production because the fiber is there. China imports enormous volumes of recovered fiber and virgin pulp precisely because its domestic forests were not scaled to meet its manufacturing appetite. When global pulp prices spiked in 2021 and 2022, Chinese corrugated manufacturers faced margin compression that smaller, vertically integrated North American and European converters avoided.

Glass packaging tells a different story. Sand for container glass needs to be the right silica purity, which is not everywhere. Italy, Germany, France, and Ohio are glass manufacturing hubs partly because the right sand is regionally accessible and the energy infrastructure to run furnaces continuously exists nearby. Glass furnaces cannot be turned off and on like corrugated converting lines. They run 24 hours a day, 365 days a year, which means energy cost and energy reliability are existential issues, not operational ones.

Aluminum for cans and closures is another example. The smelting of primary aluminum is an electricity-intensive process that concentrates near cheap hydroelectric power. That is why Iceland, Norway, Canada, and the Pacific Northwest US are aluminum production hubs. The packaging manufacturers who use aluminum sheet stock benefit from being close to these smelters because aluminum sheet is heavy, and freight costs erode margin quickly.

To see how these raw material constraints translate into real packaging supply chain operations, review the guide below.

See: How Packaging Supply Chains Actually Function from Factory Production to Final Delivery

Infrastructure: The Invisible Prerequisite That Separates Promising Markets From Reliable Ones

You can have low labor costs and abundant raw materials and still fail to manufacture competitive packaging if the infrastructure is not there. Infrastructure means roads, ports, power reliability, telecommunications, and water. All of them matter, and most sourcing analyses underweight them.

Nigeria is a textbook case. Nigeria has a large, young workforce and growing domestic demand for consumer packaged goods. Several global FMCG brands have tried to develop Nigerian packaging manufacturing capacity only to face the same wall: unreliable grid power forces factories to run expensive diesel generators, which wipes out labor cost savings. Poor road infrastructure in inland regions means raw material delivery timelines are unpredictable. And port congestion at Apapa in Lagos has, at various points, created 30-day container queues that make it nearly impossible to run a just-in-time operation.

Compare that to Vietnam, which has invested heavily in industrial zone infrastructure since 2010. The VSIP industrial parks near Ho Chi Minh City and Hanoi offer dedicated power substations, fiber optic connectivity, and rail access. A foreign packaging brand opening a factory in a VSIP zone gets a level of infrastructure reliability that would be hard to replicate by building independently in many other developing markets.

Port Capacity and the Last-Mile Problem

The packaging industry moved an estimated 14 million TEUs of finished goods in 2023 alone, according to data compiled by Drewry Maritime Research. Where a factory sits relative to a major container port is not an aesthetic choice. It is a cost driver. Every additional day of inland transit to port adds drayage cost, warehousing exposure, and scheduling complexity.

Ningbo-Zhoushan, Shanghai, Shenzhen, and Busan are the four largest container ports in the world by volume. The concentration of packaging manufacturing in China’s Yangtze River Delta and Pearl River Delta regions is not a coincidence. Those factories built their cost structures assuming sub-24-hour port access. When brands shift production to Southeast Asia, they often discover that inland logistics to ports like Port Klang or Tan Cang are less developed and add $200 to $400 per container in costs that did not exist in their China math.

Related Reading: factory-to-delivery packaging flow — How Packaging Supply Chains Actually Function from Factory Production to Final Delivery

Regulatory Environments: Why Compliance Decides More Than You Think

Regulation shapes packaging manufacturing geography for industries such as CBD boxes in two directions. In developed markets, stricter environmental standards raise production costs but also create quality floors that protect buyers from materials that could fail import testing. In developing markets, looser regulation can lower costs in the short term but create compliance risks when goods enter regulated markets like the EU or US.

The EU’s Packaging and Packaging Waste Regulation, which took effect in updated form in 2024, is already reshaping sourcing decisions. Brands selling into European markets now need to document recycled content percentages, demonstrate that their packaging and product labels for small business are recyclable or reusable, and report supply chain emissions data under the Corporate Sustainability Reporting Directive. A factory in a country without environmental monitoring infrastructure simply cannot produce this documentation. That makes it ineligible as a supplier for European-facing brands, regardless of its price point.

The US has its own set of pressures. California’s SB 54 requires that all single-use plastic packaging sold in California be recyclable or compostable by 2032, with interim milestones starting in 2025. Brands sourcing flexible plastic packaging from Southeast Asian factories that use mixed resin structures are now discovering that their cost-optimized solution creates a compliance liability in their largest market.

Tariffs as Regulatory Geography

US Section 301 tariffs on Chinese goods, which have remained largely in place through 2025 despite multiple reviews, effectively add 7.5% to 25% to the cost of packaging imported from China, depending on the Harmonized Tariff Schedule classification. For commodity formats like corrugated boxes and folding cartons, this has meaningfully narrowed the price gap between Chinese and domestic or nearshore production.

Mexico has been the largest beneficiary of this shift. USMCA-qualified manufacturing in Monterrey, Guadalajara, and the Bajio region gives brands tariff-free access to the US market with lead times of five to ten days, versus 25 to 35 days from Asian origins. Crown Holdings, Graphic Packaging, and Silgan all expanded Mexican capacity between 2020 and 2024 specifically to serve customers who were de-risking their China exposure.

Related Reading: domestic vs overseas production risks — Complete Guide to Packaging Sourcing for Small Businesses: How to Choose Suppliers, Control Costs, and Manage Domestic vs Overseas Production Risks

Geopolitical Risk: The Factor Nobody Priced In Until It Was Too Late

The packaging industry had a comfortable assumption for most of the 2000s and 2010s: geopolitical risk was somebody else’s problem, and global packaging manufacturing strategies were built on that stability. Trade would continue to liberalize. Shipping would stay cheap. Political relationships would remain stable enough that a factory in Guangdong serving a brand in Georgia was a permanent, reliable arrangement.

That assumption broke decisively between 2018 and 2023. US-China trade tensions, the COVID-19 pandemic, the Red Sea shipping disruptions of 2023 and 2024, and Russia’s invasion of Ukraine created a cascade of supply chain shocks that hit packaging hard. Resin prices spiked because ethylene feedstocks were disrupted. Liner shipping rates went from $1,400 per forty-foot equivalent unit on the Asia-to-US lane to over $20,000 at the 2021 peak. And brands that had a single-country sourcing strategy found themselves unable to fulfill.

The lesson that sophisticated packaging buyers have drawn from this period is not that offshore sourcing is bad. It is that concentration is dangerous. The most resilient sourcing strategies I have seen in the last three years are built around dual-region supply: typically a lower-cost Asian origin for standard volumes and a nearshore or domestic source for fast-turn or compliance-sensitive production.

China Plus One: What It Actually Looks Like in Practice

The ‘China Plus One’ strategy has become something of a cliche in sourcing circles, but the execution varies enormously. For packaging specifically, the ‘plus one’ option depends heavily on format. Flexible packaging formats such as mylar bags and folding cartons can be dual-sourced relatively easily because tooling costs are lower. Rigid injection-molded containers, product sleeves, and glass bottles are harder to dual-source because tooling and furnace setup costs are substantial, and minimum order quantities are high.

A mid-sized personal care brand I have been tracking since 2022 moved 40% of its flexible pouch volume from a Zhejiang province supplier to a Vietnamese factory in the Da Nang industrial zone by mid-2024. Their landed cost per thousand units increased by $12, a 6% premium. But their lead time dropped from 45 days to 28 days, and they eliminated their Section 301 tariff exposure entirely. The CFO told me the premium paid for itself in inventory carrying cost reduction within two quarters.

Technology Investment and Automation: The Wild Card That Is Redrawing the Map

Here is the part of the global packaging manufacturing story that most articles skip entirely. Automation is not coming. It is already here, and it is quietly undermining the labor arbitrage logic that sent so much production to low-wage countries in the first place, fundamentally reshaping modern packaging manufacturing.

A modern corrugated converting line from BOBST or BHS can run at 12,000 sheets per hour with one or two operators. A flexographic printing line from WINDMOELLER and HOELSCHER can produce flexible packaging at 600 meters per minute. At these production speeds, labor cost becomes a minor line item. What matters is equipment utilization, substrate cost, energy cost, and proximity to the customer.

This is why some European and North American converters are winning back business that went to Asia a decade ago. If your factory in North Carolina can run BOBST equipment at 90% utilization, your landed cost to a US customer may actually be lower than a Vietnamese factory running at 60% utilization on older equipment, once you factor in freight, lead time, and quality reject rates.

Packaging machinery brands to watch here include BOBST (Swiss, publicly traded), Barry-Wehmiller (US private), KHS (German, Salzgitter subsidiary), and Coesia (Italian). These companies are effectively writing the future geography of packaging manufacturing through their technology deployment decisions.

The Sustainability Pressure That Is Forcing a Geographic Rethink

Scope 3 emissions reporting is changing where brands want their packaging made. Scope 3 emissions include the upstream production of goods a company buys, which means the carbon footprint of your packaging factory is now, for many publicly traded brands, part of your reported emissions profile.

A packaging factory in Shandong province running on coal-heavy grid power produces significantly more carbon per unit than a factory in Germany or Scandinavia running on renewable energy. As brands face investor pressure and regulatory mandates to reduce Scope 3 emissions, this differential is starting to influence sourcing decisions in ways that the pure cost analysis would never predict.

Mondi, Smurfit Kappa, and DS Smith, three of Europe’s largest corrugated and paper-based packaging companies, have all published science-based emissions targets. Their renewable energy commitments and mill locations in renewable-rich regions are becoming a sourcing argument for European brand customers who need to document low-carbon supply chains. This is a competitive moat that Asian commodity manufacturers simply cannot replicate without massive infrastructure investment.

Frequently Asked Questions About Global Packaging Manufacturing

Why is so much packaging still made in China despite rising costs?

China has three decades of industrial ecosystem development that is very hard to replicate: deep supplier networks for resins, inks, adhesives, and substrates; a massive skilled workforce; world-class port infrastructure; and established quality management systems. Even as wages have risen, Chinese factories have invested in automation that keeps unit costs competitive. For many packaging formats, China remains the most capable option even if it is no longer the cheapest.

What makes Vietnam an attractive alternative to China for packaging manufacturing?

Vietnam offers lower wages than coastal China, USMCA-equivalent trade arrangements with major markets through the CPTPP agreement, and a rapidly improving industrial zone infrastructure. Its proximity to Chinese raw material suppliers means it can leverage existing supply chains while offering tariff and political risk diversification for US-market brands.

How much does a tariff actually change where packaging gets made?

It depends heavily on the format and the margin structure. For commodity corrugated boxes, a 25% tariff is likely to make domestic or nearshore production more competitive. For complex specialty packaging with high tooling costs and low domestic supply options, brands often absorb the tariff because switching costs are too high. The Section 301 tariffs have had their strongest geographic impact on folding cartons, flexible packaging, and polybags.

Can small brands access the same overseas factories as large brands?

Not always directly, but often through consolidators and trading companies. A factory in Guangdong that has a minimum order quantity of 50,000 units per run may work with a trading company that aggregates orders from multiple small brands. The trade-off is less direct quality control and slightly higher per-unit cost due to the intermediary margin. Platforms like Alibaba and specialized packaging sourcing agents can help small brands navigate this, though due diligence on factory certification and audit history is critical.

What role does currency volatility play in packaging sourcing geography?

A significant one that is often invisible until it hurts. If you are paying a Vietnamese factory in USD and the Vietnamese dong weakens, you might benefit temporarily through lower quoted prices. But if the supplier’s raw material costs are denominated in USD (which most petroleum-derived resins are), the benefit disappears. Currency mismatches between what factories pay for inputs and what they charge for outputs create price instability that can blow up a cost model over a multi-year contract.

Are there packaging formats that will always be made close to the end market?

Yes. custom cardboard boxes for e-commerce are a strong example: they are bulky relative to their value, and the logistics cost of shipping them long distances erodes any manufacturing cost advantage. Fresh produce packaging also tends to be regional because the packaging needs to move with the product on short timescales. Glass bottles for local craft beverage producers are another example, since minimum order quantities and freight costs often make local or regional production the only practical option.

What This Means for How You Source Packaging in 2026

The geography of global packaging manufacturing is not static. It is being actively reshaped by four forces that did not exist in their current form even five years ago: US-China tariff structures, EU sustainability regulation, post-pandemic supply chain risk awareness, and the accelerating deployment of automation technology in developed-market factories.

The brands and procurement teams that will win over the next decade are the ones who stop treating packaging sourcing as a cost optimization problem and start treating it as a strategic capability. That means building relationships with suppliers in multiple regions, understanding your compliance exposure in your target markets, and modeling total landed cost rather than factory gate price.

There is no single right answer to where your packaging should be made when building a long-term customized packaging solution. But there is definitely a wrong answer: letting inertia or the last purchase order decide it for you without understanding the forces that are shifting the ground underneath every sourcing relationship in this industry.

What geographic shifts are you seeing in your own packaging supply chain? I would be genuinely interested to hear whether the patterns described here match what you are experiencing on the ground.